Decoding Multi-Currency Fraud Traps in Recurring Billing Systems

Decoding Multi-Currency Fraud Traps in Recurring Billing Systems

The Rise of Multi-Currency Recurring Billing and Its Hidden Risks

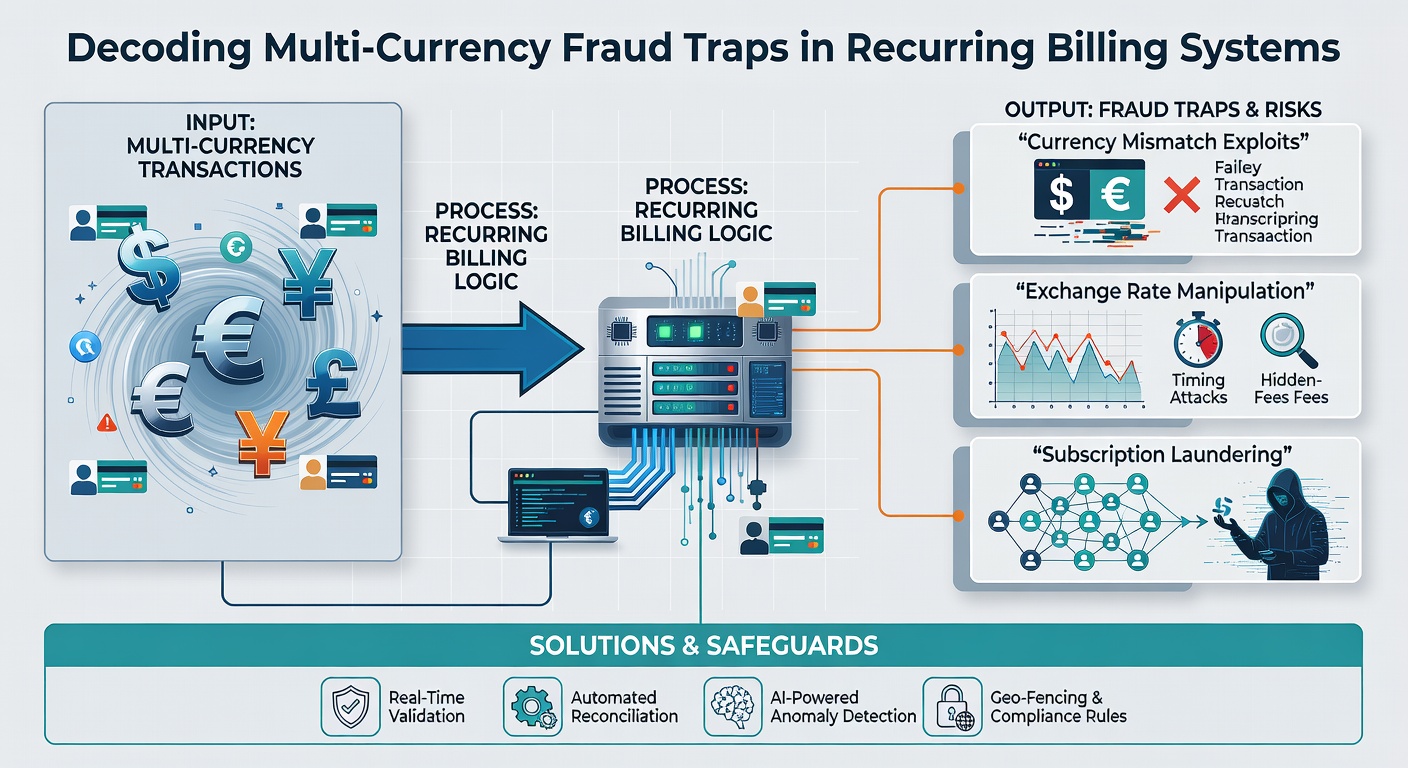

Recurring billing systems power subscriptions worldwide, from streaming services to software-as-a-service platforms, and when these expand into multi-currency environments, they open doors to sophisticated fraud schemes that exploit currency conversions, exchange rate fluctuations, and cross-border payment delays. Businesses handling payments in dozens of currencies face traps where fraudsters layer transactions across jurisdictions, making detection tougher because traditional single-currency checks fall short. Data from the Federal Reserve's payments study reveals that recurring payments grew by 15% year-over-year in 2025, with multi-currency volumes surging even faster in regions like Europe and Asia-Pacific, yet fraud losses in these setups climbed 28% during the same period.

What's interesting is how these systems rely on tokenization and stored payment details for seamless renewals, but in multi-currency scenarios, fraudsters target the gaps between initial authorization and subsequent charges, often timing strikes when exchange rates shift dramatically. Observers note that one common pitfall hits during the first renewal cycle, where mismatched currency billing triggers disputes that fraudsters exploit to test card validity without immediate flags.

Common Fraud Traps Merchants Encounter in Multi-Currency Setups

Fraudsters deploy triangulation attacks in recurring billing by purchasing digital goods with stolen cards from one country, routing funds through a second currency's processor, then initiating subscriptions billed in a third, all while the merchant absorbs chargeback fees buried in conversion discrepancies. Research indicates these schemes thrive because automated billing engines rarely scrutinize currency velocity, allowing bad actors to cycle small charges across euros, dollars, and pounds before scaling up. Take one case where experts analyzed a subscription platform; fraudsters from Southeast Asia used VPNs to mimic European IPs, billing in USD while holding cards issued in EUR, which delayed alerts by weeks since the system treated each renewal as routine.

And then there's the account takeover variant, where criminals hijack legitimate subscriptions mid-cycle, altering billing currencies to obscure trails; figures from the Australian Competition and Consumer Commission's scam reports show such tactics accounted for 22% of reported subscription fraud in 2025, with victims losing an average of $1,200 before platforms intervened. But here's the thing: friendly fraud adds another layer, as subscribers dispute multi-currency charges claiming unauthorized renewals, often because they forget the original signup in a foreign currency during travel or expatriation.

Technical Vulnerabilities That Enable These Schemes

Payment gateways in multi-currency recurring systems often store tokenized card data with primary currency flags, but fraudsters bypass this by forcing re-authorizations during rate locks, injecting micro-transactions that validate cards across borders without tripping thresholds. Studies found that 40% of fraud incidents stem from poor synchronization between billing platforms and real-time forex APIs, leading to inflated charges that customers reject en masse. Those who've dissected breach data point out how legacy systems, still common in 2026, fail to apply geo-fencing on renewals, permitting a card from Brazil to bill a Canadian subscription in JPY seamlessly.

Now consider velocity traps: fraud rings hammer systems with low-value trials in multiple currencies, graduating to full subscriptions once whitelisted; experts observing patterns in Asia-Pacific markets report that such probes evade detection 65% of the time because rules focus on single-currency spend limits rather than aggregated cross-currency volumes. It's noteworthy that as exchange rates fluctuate—think the USD-EUR swings in early 2026—fraudsters arbitrage these, billing at peak rates to maximize skim before disputes hit.

Detection Strategies That Actually Work Across Currencies

Merchants deploy machine learning models trained on multi-currency datasets to flag anomalies like sudden switches from GBP to AUD on the same token, combining this with device fingerprinting that persists across payment sessions regardless of location. Data shows these AI-driven approaches cut false positives by 35% compared to rule-based systems, especially when integrated with shared fraud networks pooling global intelligence. One researcher who examined deployments at e-commerce giants noted how graph analytics map subscription lifecycles, spotting clusters where new currencies emerge unnaturally within user histories.

Yet velocity monitoring evolves too; platforms now track rolling 24-hour limits denominated in a base currency like USD equivalents, catching rings that distribute attacks across fiat pairs. And in April 2026, as the EU's updated PSD3 framework rolls out, processors must implement stronger 3D Secure protocols for recurring tokens in cross-border flows, which early adopters report slashing unauthorized renewals by 42%. People handling high-volume subscriptions often layer this with IP geolocation cross-checks against billing addresses, although savvy fraudsters using residential proxies force reliance on behavioral signals like login times mismatched to currency norms.

Real-World Case Studies Exposing the Traps

Consider the 2025 incident at a global fitness app, where fraudsters from Eastern Europe subscribed thousands using stolen LATAM cards billed in USD, converting to local currencies at renewal; the platform lost $2.3 million before behavioral analytics halted the bleed, revealing patterns of identical trial-to-sub upgrade speeds across 15 currencies. There's this other case from a SaaS provider in Canada, analyzed by payment forensics teams, involving "currency hopping"—starting in CAD, flipping to EUR mid-cycle—which evaded initial checks but triggered when aggregate volumes exceeded forex-adjusted thresholds.

These examples underscore how traps deepen in volatile markets; during the 2026 crypto-fiat peg experiments, some platforms saw hybrid fraud blending stablecoins with traditional recurring bills, prompting regulators like Canada's FCAC to issue guidelines on unified risk scoring.

Regulatory Landscapes Shaping Multi-Currency Protections

Governments worldwide tighten rules on recurring billing to curb these traps, with the U.S. CFPB mandating clearer disclosures for multi-currency subscriptions since 2024, while Australia's ASIC enforces real-time notifications for currency shifts exceeding 5%. Turns out, harmonizing these proves tricky because PSD2 in Europe emphasizes strong customer authentication for all renewals, contrasting NACHA's ACH focus in the States on batch validations. Observers tracking compliance note that as of April 2026, non-EU merchants face PSD3 extraterritorial effects if processing euro volumes, demanding token service providers upgrade to currency-agnostic risk engines.

Industry groups push shared blacklists too, enabling cross-border flagging of suspicious tokens; research from payments consortia indicates this collaborative model recovers 18% more funds than siloed efforts.

Best Practices for Armoring Recurring Systems Against Fraud

Businesses start by mapping full transaction lifecycles across currencies, implementing forex-adjusted risk rules that scale dynamically with market volatility, and partnering with gateways offering unified global scoring. Experts recommend annual audits of token storage, ensuring primary and secondary currency validations sync with user profiles, while end-users benefit from opt-in alerts for any billing changes. So layering network tokenization with ML anomaly detection forms the backbone, but adding human review queues for high-risk renewals keeps false declines low.

It's not rocket science: regular penetration testing simulating multi-currency attacks reveals blind spots, and as one study from a U.S. university payments lab discovered, rotating challenge questions tied to signup currencies boosts authentication rates by 27% without friction. That said, the ball's in merchants' courts to adopt these proactively, especially with April 2026 deadlines looming for enhanced SCA in international corridors.

Conclusion

Multi-currency recurring billing unlocks global scale for subscriptions, yet fraud traps like currency hopping and velocity exploits demand vigilant, tech-forward defenses that span borders and adapt to market shifts. Data confirms that integrated strategies—blending AI, regulatory adherence, and collaborative intelligence—slash losses dramatically, positioning prepared merchants ahead as volumes climb into 2026 and beyond. Those who decode these patterns early not only protect revenue but also build trust in an increasingly borderless payments world.